Securing a home loan remains a hurdle for small businesses, according to Great Southern Bank’s Smaller Small Business Research.

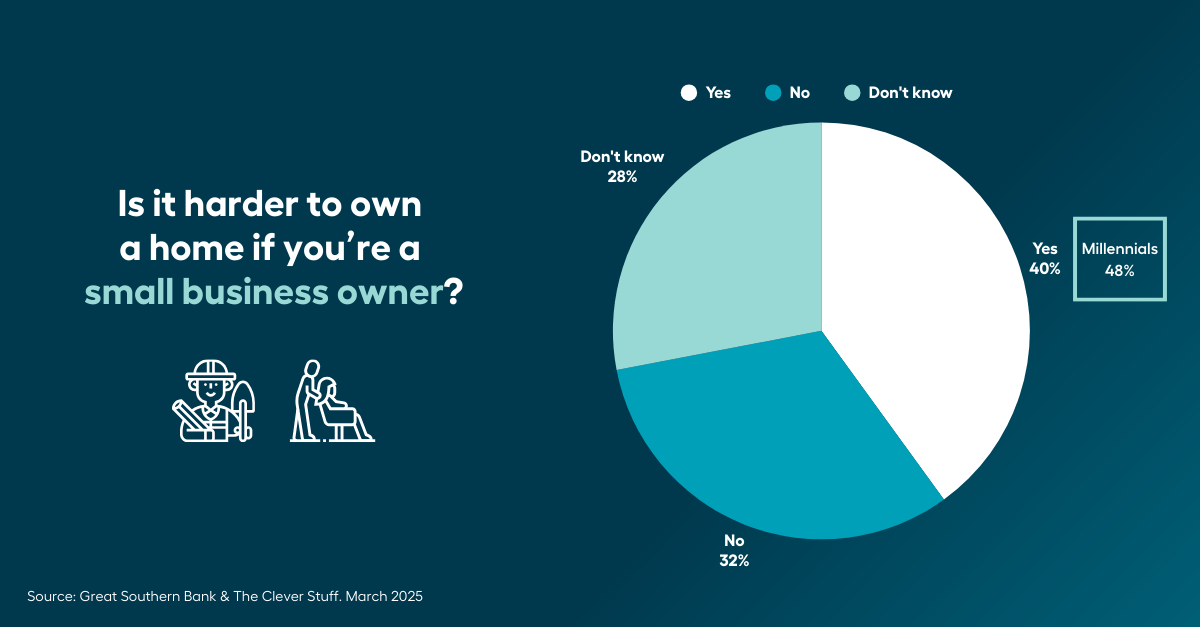

20% of small business owners reported they are still saving for a house deposit, with 40% believing being self-employed makes it harder to own a home.

Income instability topped the list of unique challenges, followed by lending criteria, being labelled ‘high risk’ by lenders and obtaining the right paperwork.

For millennials these challenges were much more apparent with nearly half (48%) of small business owners aged between 27 and 42 stating they were challenged.

Understanding the needs of small business owners, Great Southern Bank has enhanced its lending policies to enable sole traders a simplified process for home loan approvals.

Bank insider insight: What lenders are really looking for

Jacole Davies a mortgage broker at Aussie Redcliffe specialises in assisting self-employed clients with a home loan and explains: "Lenders want consistency in income, and that can be tough for business owners whose earnings fluctuate."

Above all else Jacole says proving consistent income over the last two years is where all small business owners should start.

“All too often I come across applicants who just aren’t paying themselves first, or enough of a wage and placing that income into the business – that will impact your borrowing power,” Jacole explains.

Tips for self-employed to master homeownership

-

Pay yourself first, and regularly: A steady income stream signals stability. Borrowers should always ensure they are paying themselves first and across a regular pay cycle.

-

Clean up debt, don’t add to it: Reduce personal debt before applying to boost your debt-to-income ratio.

“Many clients think that taking out a car loan will improve their credit score prior to applying but it does the opposite, lowering your serviceability,” explains Jacole.

-

Organize your paperwork– or have someone do it for you: While some lenders may require less, aim for having two years of tax returns (Notice of Assessments), Business Activity Statements (BAS), and financial records at the ready. This is often where a good accountant plays a key role.

-

Addbacks - the more financial detail, the better: Addbacks are expenses which can be added back into a self-employed applicant’s income, for assessing serviceability of a mortgage.

Jacole explains: “These are commonly found within tax returns or profit and loss statements and can be assessed according to the funder’s policies by an experienced broker.”

Common examples are depreciation, including asset and interest write offs, non-compulsory superannuation, non-recurring expenses and ceased financial commitments.

Lending a hand to smaller small businesses

Brendon Prior, Senior Manager Broker Performance at Great Southern Bank explains the bank has recently enhanced their self-employed policies to simplify the paperwork required for home loan approvals.

“With the help of our broker BDM network, we aim to take more of a commonsense approach when evaluating consistent income for sole traders.”

“For sole traders, we are one of the few lenders who will can assist with home loan lending if they have been in business for less than two years - requiring their most recent Notice of Assessment and two Business Activity Statements (BAS), provided they are not less than 90 days old,”

“We also encourage small businesses who have significant qualifications and work experience in their trade to talk to us – this can be taken into account for the two years prior to starting in business, if income has been consistent.”

To further support smaller businesses Great Southern Bank recently launched its Business+ app.

“The Business+ app offers banking and financing for small businesses. It includes bank feeds to MYOB and Xero and a free invoicing tool with automated payment reminders to help business owners reduce admin and save time.

“The platform makes it so much easier for small businesses to track and prove their income and expenses, especially handy to have in one place with your bank when you are having financial conversations.”

Great Southern Bank’s Smaller Small Business Research was undertaken in partnership with The Clever Stuff in November 2024 with 1500 Australian small businesses with 10 employees or less.