Globally, green loans and sustainability-linked loans have been growing rapidly in the past few years – as society becomes more conscious of their environmental footprint (and those of the companies they use and invest in, too). Annie Kane takes a look at green loans, and what they can be used for.

In early August, shocking headlines hit the global press.

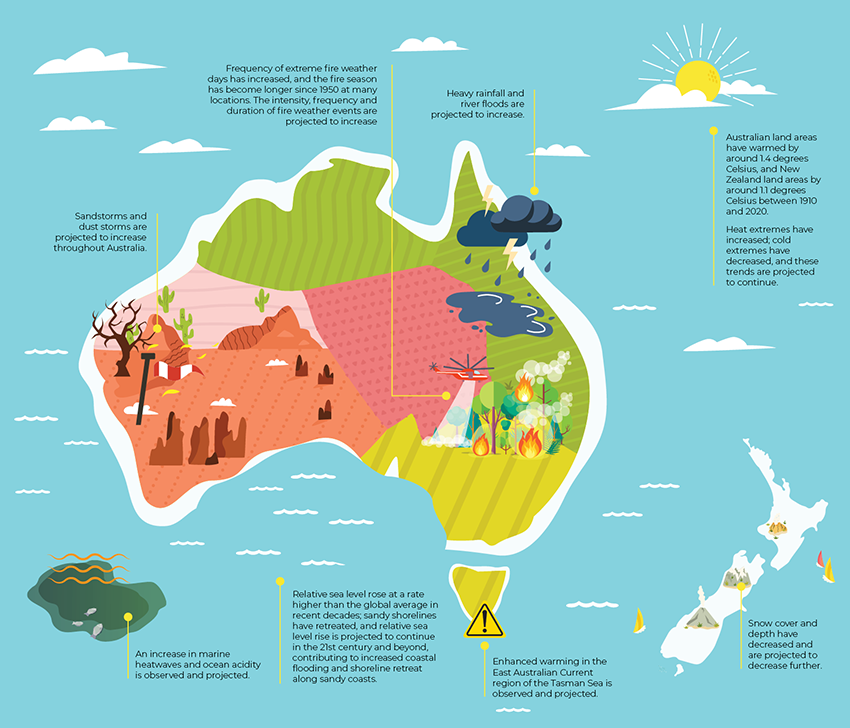

The UN’s body for assessing the science related to climate change released its devastating sixth report, outlining the very real (and terrifying) state of the global climate. The Intergovernmental Panel on Climate Change (IPCC) report – written by 234 authors from 66 countries – provided the most up-to-date understanding of the climate system and climate change.

The first of several reports from the IPCC’s three working groups revealed that scientists are observing changes in the Earth’s climate in every region and across the whole climate system.

It told us what many already knew but wish to ignore – changes observed in the climate are unprecedented in thousands, if not hundreds of thousands, of years, and some of the changes already set in motion (such as continued sea level rise) are irreversible over hundreds to thousands of years.

The report shows that emissions of greenhouse gases from human activities were responsible for approximately 1.1 degrees Celsius of warming since 1850-1900, and estimates that – when averaged over the next 20 years – the global temperature is expected to reach or exceed 1.5 degrees Celsius of warming.

In the coming decades, climate changes will increase in all regions. With 1.5 degrees Celsius of global warming, there will be increasing heat waves, longer warm seasons and shorter cold seasons. At 2 degrees Celsius of global warming, heat extremes would more often reach critical tolerance thresholds for agriculture and health, the report shows.

“This report is a reality check,” said IPCC Working Group I co-chair Valérie Masson-Delmotte.

“We now have a much clearer picture of the past, present and future climate, which is essential for understanding where we are headed, what can be done, and how we can prepare.”

“It has been clear for decades that the Earth’s climate is changing, and the role of human influence on the climate system is undisputed,” she added.

But there is hope. It noted, for example, that strong and sustained reductions in carbon dioxide (CO2) emissions and other greenhouse gases would limit climate change.

“Stabilising the climate will require strong, rapid and sustained reductions in greenhouse gas emissions, and reaching net zero CO2 emissions. Limiting other greenhouse gases and air pollutants, especially methane, could have benefits both for health and the climate,” said IPCC Working Group I co-chair Panmao Zhai.

Greening the home

While the greatest impact in reducing emissions would be from a national/governmental level, there is a groundswell of action coming from individuals wishing to reduce their emissions and carbon footprint.

But it’s not just Greta Thunberg’s followers taking action, it’s everyone. Whether it’s Millennials concerned about what the world will look like when they retire, Baby Boomers thinking about the legacy they’re leaving their grandchildren, or those recovering from the devastating bushfires and drought vowing to do their part to help reduce extreme events – individuals across Australia are looking at ways of reducing their own emissions and supporting more companies who do something about theirs, too.

One of the most effective ways the average consumer can reduce their footprint is through their home and transport choices. The built environment makes up approximately 23 per cent of Australia’s carbon emissions – with around 13 per cent coming from houses – so building energy-efficient or solar passive homes can go a long way in reducing the total CO2 load in this country.

For home owners already living in – or looking to buy – existing property, there are a growing range of products available to help them reduce their emissions too. This can include installing energy-efficient products (such as water recycling or solar panel heating) and making more efficient design/architectural choices (such as wall/ground insulation). These not only help them reduce heating/air-conditioning “leaking” from the houses (which in turn requires more energy to be used to create heat/cooling) but also helps increase renewable energy generation.

As with any purchase, though, there is the question of financing it. Enter green loans. While green loans can refer to both corporate loans/investments, for the average borrower it refers to a finance product that enables them to purchase or install the products and services necessary to reduce their carbon footprint.

- Personal loan products that specifically enable Australians to purchase and/or install environmental upgrades to their home are commonplace now, and can be used for things such as:

- Solar and photovoltaic panels

- Solar battery storage systems/electric vehicle charging stations

- Solar or gas hot water systems

- Solar pool heaters

- Solar hydroponic heat pump systems

- Rainwater tanks

- Water pumps

- Grey water treatment systems

- Home insulation that meets government standards for geographic area Certified double glazing for windows

- Split systems, evaporative cooler or star-rated zoned air-conditioning units with either a minimum energy rating 4/6 stars or minimum 6/10 stars

- Energy-efficient LED lights.

In the past year alone, several lenders have been issuing new green loan products to help keep up with demand, with non-bank lender Plenti even launching a buy now, pay later (BNPL) finance option for the installation of residential renewable energy technology (such as solar panels and batteries) in March of this year.

The product enables home owners to make interest-free monthly payments for a fixed monthly fee of $5.99 over three to six years, while the cost of extending finance is paid by the renewable technology vendor through an upfront merchant fee, as per the arrangement with other merchants providing BNPL.

Plenti piloted the product before launch to gauge appetite and found that, during this period, solar finance applications through pilot partners have increased by 80 per cent when compared with the average demand in the previous six months.

Non-major banks – and particularly the mutuals (which have typically prioritised environmental, social and corporate governance criteria) – have also been busy providing new green loans to their customers.

Bank Australia was the first home loan provider to receive finance from the Clean Energy Finance Corporation (CEFC) to offer a green loan. Launched in January 2020, the Bank Australia Clean Energy Home delivers discounted interest rates to qualifying builders and home buyers.

The $60 million of CEFC finance for the loan was expected to be used by 70 customers in its first year – with the total pool expected to be used within 18 months. However, strong demand for it saw the bank attract 140 customers in the first 12 months, with CEFC later extending its commitment to $90 million due to the strong take-up.

According to CEFC, 60 per cent of the applicants used the funding to build a new home, 35 per cent made property upgrades and 5 per cent opted to achieve high energy efficiencies to be eligible for a larger discount (but this part of the scheme was later dropped, to “simplify the overall product”).

More lenders have been issuing their own discounted green loans this year too.

In May, Gateway Bank announced new additions to its range of environmentally conscious products and services, including discounts on its Premium Package mortgage products if they have environmentally sustainable homes.

Those on a Premium Package offering (for loans of between $250,000-$2 million on an 80 per cent loan-to-value ratio) can access a discount of 0.15 per cent if their home has at least three eligible green aspects, meaning rates on Green Home Loan start from 2.44 per cent (2.78 per cent comparison).

Similarly, under the Green Plus Home Loan, borrowers are able to access a discount of 0.25 per cent on the Premium Package if their property has a Nationwide House Energy Rating Scheme (NatHERS) rating of 7 stars or higher (evidenced by a NatHERS Certificate completed by a NatHERS certified assessor) or equivalent (for those in the ACT, which has its own system).

Rates on the Green Plus Home Loan start from 2.34 per cent (2.69 per cent comparison).

Speaking about the new offerings, Gateway Bank CEO Lexi Airey commented: “Generally, we’ve found that if you want to be green and you want to do something good, it’s going to cost you a bit more.

“So, what we wanted to do was to look at how we could provide products that allow you to be green, do the right thing, but also get rewarded for it.

“With the new green home loans, we’re recognising those who are making a step on the journey of sustainability and rewarding that.

“As the famous philosopher Kermit the Frog said: ‘It’s not that easy being green’. So, we’re trying to help.”

The majors are also getting on board. Australia’s largest lender, the Commonwealth Bank of Australia (CBA), also recently rolled out a new CommBank Green Loan for new and existing customers with an eligible CommBank home loan.

Secured against an existing CBA mortgage, the green loan enables eligible customers to borrow up to $20,000 in renewables at a fixed rate of 0.99 per cent per annum. It can be repaid over 10 years and has no set-up monthly service or early repayment charges (though late payment fees would apply).

Since launching the product (which first rolled out in pilot in February 2021 before fully launching in July), CBA has funded, or is in the process of funding, nearly $4 million worth of clean energy products since the offering has been available – and estimates that customers have reduced emissions by 60 tonnes.

CBA group executive Angus Sullivan said: “With over 11 million retail customers and more than 25 per cent of the home loan market with the CBA Group, we have a responsibility to provide solutions for customers that reduce their environmental impact, and the green loan is an important step towards helping our customers and communities move to cheaper, clean energy technologies.”

The major bank is now looking at other means to enable customers to reduce their environmental footprint as part of its climate strategy, including “actively exploring” the option of solutions for electric vehicle financing as customers are looking for this.

He said in July: “The green loan is our first customer-facing product, and I’m excited because we have been doing a lot of work in this space and have some exciting announcements coming.”

With the IPCC report renewing the focus on sustainability, and more lenders offering products to meet consumer demand for green loans, now is a great time for brokers to be talking to their clients about how they intend to finance their actions to help secure a greener future.

[Related: CBA launches green upgrade for commercial mortgages]