Powered by

MOMENTUM

MEDIA

Commercial lending is fast becoming a hot market for brokers looking to grow their business in an ever-shifting financial landscape. Those who do break into the market stand to not only significantly bolster their brokerage’s offering, but also “double, if not triple” their potential revenue stream, as ING DIRECT national partnership manager, third-party commercial, John Kolyvas, points out.

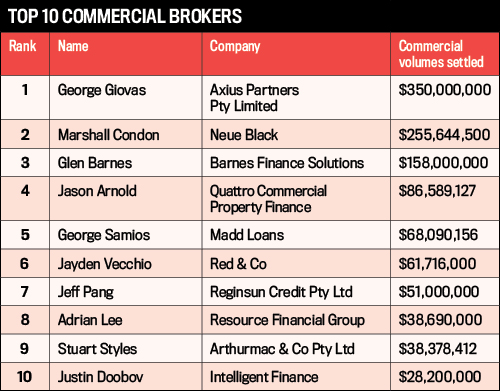

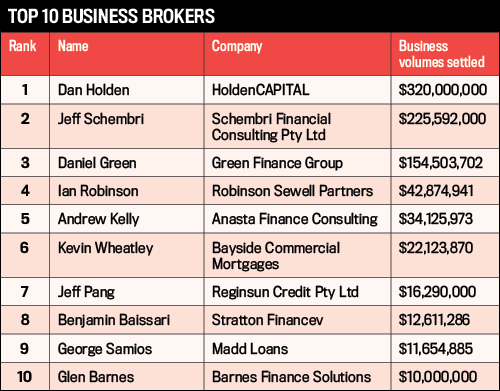

Savvy brokers are clearly catching on to the significant benefits that await them in this space, as the volume of commercial loans written by those at the top of the ranking increased from $141 million (commercial) and $164 million (business) last year to $320 million and $350 million this year.

Neue Black founder and CEO Marshall Condon, who placed second in the Business Writers ranking, emphasises that playing in the commercial lending space can bring brokers a range of diverse experiences.

“In the commercial space, no deal is the same as the last, they all have their unique areas attached to them. Each new deal is another challenge, so there is something satisfying about being able to understand what the client is looking for and be able to deliver on that,” he says.

“Through different sources and through doing different things, we’re always increasing in knowledge and experience by taking those transactions; it’s the new frontier,” he adds.

The results of a poll conducted by The Adviser show that a growing number of brokers are adding commercial lending to their portfolio. A whopping 68 per cent of brokers surveyed said that up to a quarter of their total loan book comprises commercial loans, while 13 per cent said it makes up between a quarter to half of their business, and 12 per cent revealed that it makes up between 75 to 100 per cent of their workload.

So, what does it take to join these brokers and achieve success in this dynamic and lucrative market?

""WE'RE ALWAYS INCREASING IN KNOWLEDGE AND EXPERIENCE BY TAKING THOSE TRANSACTIONS; IT'S THE NEW FRONTIER"

Building a solid network

Neue Black’s Mr Condon, who started out in the industry straight out of high school, says that he learnt from a young age that when it comes to commercial broking, “building a network is very, very key”.

“To get those opportunities to do those deals, it’s about getting someone to trust you and like you and want to give you the opportunity,” he says.

Mr Condon says that, for younger brokers especially, starting out in the commercial space requires them to “dig in and put in the work”.

“Build your network to get those opportunities because the needs of a business customer are much different to a home loan customer,” he advises.

“Opportunities come [on occasions] when the client’s current bank can't give them what they're after, so you need to be already in the client’s network or know someone within that network who they can refer to you from there.

“It's a very, very long game to get into unless you're in that stage or have clients yourself, so need to build a network,” he concludes.

“Measure four times, cut once”

HoldenCAPITAL’s Daniel Holden, who topped the business loans writers ranking, emphasised that “the numbers are substantially higher” in the commercial lending space, and thus a higher degree of accuracy and attention to detail is required.

“A home loan could be $400,000 or something, whereas the average commercial loan that we do is somewhere around $7 million or $8 million and that's generally involved in a project that is anywhere from $15 million to $50 million, so if you get it wrong, you've got a lot more to be accountable for.

“So, it's imperative that you're on your A-game and delivering good service and good product.”

Over the past year, we’ve seen a surge in commercial applications, as brokers have strived to highlight to their clients the opportunities for building wealth in the commercial sector. In line with this growing trend, we’ve focused on giving our brokers the support necessary to leverage commercial opportunities. We’ve expanded our commercial sales and credit risks teams, have expanded our credit appetite to include larger and more complex transactions, and have embarked on an aggressive commercial loan growth project to further establish our presence in the commercial lending market.

Mark Woolnough, ING DIRECT’s head of third-party distribution

Having featured in the commercial business writers ranking every year since its inception, the successful broker talks about his background in broking and shares some of the secrets to his success

Q. What attracted you to the broking industry?

I started broking straight out of school. I moved down to Melbourne to go to university to get an economics degree and got offered a role in a broking firm in February that year.

I didn't know what a mortgage broker was when I first started. The reason why I took the role was I wanted to get some experience while I was doing my degree, but I got a start in the finance side of things and once I started working there I found I was doing really well and enjoyed it so I decided to do it full-time.

Q. You've featured in the ranking every year since it started, so what have you been doing to consistently stay at the top of your game?

I think every successful broker is really, really good at building and maintaining relationships, whether that be with their client or their supplier, and they're generally able to have a very strong working relationship where it's mutually beneficial for both parties so one thing I pride myself on is the relationship I have with my clients.

Q. In terms of commercial broking, how easy is it for new brokers to play in this space?

I think the [broking industry] is not seen as it was previously by the consumer, and the numbers point to that with 52 per cent of loans being introduced via brokers now. In the commercial space, however, it's much less; I think it's less than 20 per cent, and that's because the types of transactions are different. In the business space, it is relationship based, and when a client has all their business banking and loans with a certain banker, it's not as easy as getting a certain price to move them across. It's really going to affect their business, so it's a big decision.

Q. What are the main benefits of adding commercial lending to your portfolio as a broker?

The main benefit is that it does spread your network to a different type of clientele than potentially a residential client. The businesses that we work with, the people are generally more wealthy, so there's a bit more money behind them. The referrals we get from most clients are generally higher calibre and larger home sizes, so the majority of the home loans we do for our business customers are generally seven figures, which increases our residential loan sizes.There’s also the diversity. In the commercial space, no deal is the same as the last, they all have their own unique areas attached to them, so each new deal is another challenge to try and overcome and to get placed.

The project

[We had] one in West End [Queensland], which was 106 apartments. The project was called Citron. An existing client of ours was taking the project. We had issues with the company that was contracted initially, and we had to manage that with one of the big four banks who did the funding. We negotiated that on behalf of the developer and managed the process of removing the existing bankrupt builder and replacing them with a new contract and a new builder.

The challenge

Having a builder go broke on a $24-million building contract with construction is definitely a big challenge. Negotiating with the bank to keep them interested in the deal, and on track, and heading towards the finish line, was definitely difficult considering the change in funding appetite… They funded the budget [but there was] now the opportunity where they could have potentially walked away. That was definitely the biggest challenge I've had this year, but also the most rewarding.

The outcome

It was quite cumbersome and a little bit tedious for the developer because you don't expect the builder to go broke just after you've engaged them. So managing that process and seeing that we still managed to get that result and keep the bank on board and get the project up and running again was definitely a highlight.

The regional broker wrote over $42 million in business loans this year. Here he gives some insight into how he does it

Q. Are there any unique difficulties involved with doing business loans as a regional broker?

The challenges are threefold. First, there isn’t the population density that correlates with having access to a deeper pool of prospective clients. This leads to the second challenge being the tyranny of distance that must be covered to access your target audience. Travelling interstate is common in our line of business. Third, regional and rural Australia tends to be more conservative towards outsourcing the talent required to negotiate funding requirements for their respective business. This is more an issue of educating the audience around the inherent complexity of commercial lending, and the necessity to refine their presentation to access maximum leverage from their engagement with the banks.

Q. How do business loans differ from residential loans – what are the main differences?

Commercial loans operate at the sophisticated end of the spectrum with regards to loan assessment. Every industry and enterprise is uniquely different which must be analysed from a feasibility and sensitivity perspective. The risk analysis must be technically detailed to allow credit the comfort in supporting each transaction. Most commercial transactions we deal with take more than six months to refinance. The runway is long and that disguises many unforeseen challenges prior to any settlement is achieved.

Q. What was your biggest business deal this year?

I have recently settled a $11-million transaction that involved multiple entities engaged in a bio-waste management enterprise, and I am also about to refinance a beef production enterprise for $15.8 million.

Q. What did you enjoy most about it?

An incredible amount of satisfaction was gleaned from the client’s response. Not only from the six-figure per annum savings that we achieved from the process, but probably more so from his realisation that a borrower could access such professional services in comparison to the sheer lack of service they were receiving from their encumbered bank (their bank manager resigned and they did not have a bank manager for six months to assist them with their expansion).

Q. What was your most challenging business deal this year, and how did you navigate it?

A young couple seeking a $2.5-million construction and operational finance for a green-field regional project that had no trading history. Their existing bank and another major bank they approached both declined their proposition so the initial proposition was not strong. I had to reconstruct their funding proposition to mitigate all the policy risks, and create funding structures that would be more palatable for the banks to consider. It also involved cross border trade finance given a lot of the machinery was being sourced from overseas. With the right presentation and selecting the right deal team within a major bank the deal was approved and funded. The borrowers were extremely happy.

Q. For other brokers (particularly other regional brokers) who may be interested in breaking into the commercial space, what advice would you give them?

My main advice is to ensure you incrementally build up your knowledge and skill set slowly as you move through the complexity of the commercial lending spectrum. Going in too deep, too early may damage your reputation permanently – and reputation and integrity within regional areas is the foundation of your business.